The most notable change this month is that months of inventory (MOI) tightened for entry-level detached homes in popular suburbs.

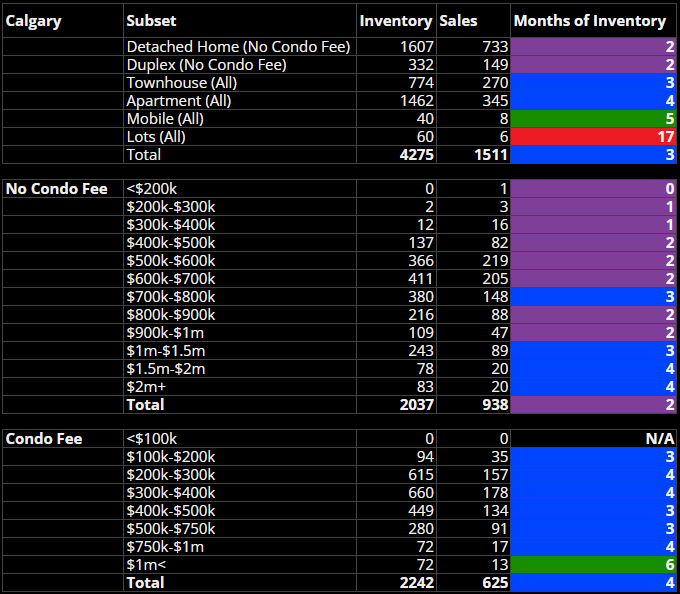

Calgary continues to behave like several different markets at once. The broad statistics tell one story, but once you break the numbers down by price range and location, the reality becomes much more nuanced.

One additional note this month: the war in the Middle East is an obvious “elephant in the room” for Alberta’s economy. It is far too early to judge how it might ultimately affect our housing market. Higher oil prices could support Alberta’s economy and housing demand, but global instability could also slow economic activity or influence interest rates in ways that offset that benefit. At this stage, we are simply watching.

For our Calgary readers, this might also be one of those rare months where it is worth briefly glancing at the Fort McMurray section. That market can occasionally act as a bellwether for Alberta’s energy-linked housing cycles, and some interesting signals are beginning to appear there. As for Calgary, let's get into it!...

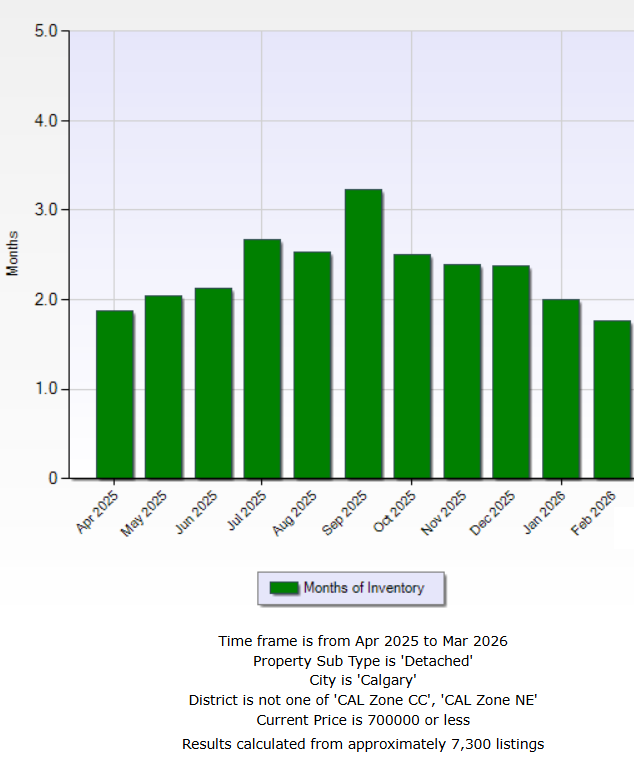

Here's the chart for months-of-inventory for detached homes under $700,000:

Let's start the analysis with why the market for entry-level detached homes is tightening:

- We started the year with low inventory

- Early spring demand is beginning to appear

- Slightly stronger buyer confidence than this time last year in those price ranges

This supply-demand imbalance is particularly obvious under $600,000, where I bumped into other buyers (multiple-offer situations) a few times. That being said, the culture of the detached market as a whole remains balanced. Many buyers are still choosing to avoid multiple-offer situations if possible and will move on to the next listing rather than compete.

If tight supply continues, however, that culture will have to change - at least in those price ranges, ultimately causing prices to rise.

The rest of the market:

- Apartments are firmly in a buyer's market, with declines in values expected.

- The townhome market is highly location-dependent - suburban new construction areas are in a buyer's market, whereas central properties are very stable.

- Pockets of mid-market detached homes are seeing continued declines. This is largely driven by confidence, as there is often very little actually for sale.

- New construction areas are seeing price declines.

- The most prime pockets of the Inner City are seeing (I believe) appreciation.

- The market for luxury homes is complex - positive and negative surprises occur, but they are mainly correlated to location and newness. In particular, super-prime locations are selling very well.

- Cochrane and Airdrie are experiencing buyer's market conditions, whereas Okotoks is balanced.

Reading the bullets above can feel contradictory, but that’s because broad market statistics hide what is really happening on the ground.

- The differences between micro-markets are so significant that broad conclusions can often be misleading. We really do need to look at families' goals and homes and give precise, tailored suggestions - and even then, months of inventory alone isn't always a good predictor of a listing outcome...

- If an alien came and looked only at months of inventory (MOI), they might assume two neighbouring neighbourhoods would behave the same way. However, the devil is in the details. Both markets might appear to have no competition, and the alien might suggest listing the home at a high price. In one market, recent sales may have all occurred in multiple-offer situations; in the other, listings may have required price reductions before selling. Both markets might technically have rising MOI levels, but due to differing levels of buyer confidence, one remains stable while the other declines. More than ever, we need to look at pricing (including both recent sales and current competition), MOI, price trends, as well as days on market and discounts.

It’s fascinating for us to be operating in such a complex environment. Our clients sometimes come to us with a clear picture of what is happening; often, they don’t. Because things are so nuanced, we encourage regular micro-assessments of the property type, price range, and location where you are planning to transact.

We regularly provide mini pricing documents and market assessments (going up or down and why) for clients across the region. Please reach out if you'd like an update!